China’s Economic Shift: Moving Away From Global Integration

We’re going to spend December looking ahead at 2024’s prospects. We have an optimistic outlook for many global markets: in coming weeks we’ll describe why we’re bullish on Japan and India in particular, as well as giving our outlook on the United States.

But today we’ll start with perhaps the murkiest of our year-ahead interests: China. What is the general landscape for investors in China? With Chinese markets in the doldrums, do we see opportunity, or a red flag? To tip our hand, we don’t generally view China as fertile ground for investors (more about that below) -- but its outsized influence on global markets and economies means that it’s essential to watch. That’s a major reason why we write about it.

China Downgrade

A topic we’ve been mentioning for years -- China’s slow-motion descent into the economic troubles brought about by overleverage, deteriorating domestic policy, and geopolitical tensions -- is entering more deeply into the mainstream. On Tuesday, Moody’s revised its outlook on China’s government credit ratings to negative from stable. This change underscores the global concern over rapidly rising local government debt and the deepening property crisis in the world’s second-largest economy; this suggests the need for greater financial support for debt-burdened local governments and state firms, presenting broad risks to China’s fiscal, economic, and institutional strength.

The situation is further complicated by persistently lower economic growth and ongoing retrenchment in the property sector. China’s equity markets have fallen to nearly five-year lows, reflecting concerns about the country’s growth trajectory (as well as a lack of domestic appetite for speculation, which is one of the primary drivers of the Chinese stock market). The cost of insuring China’s sovereign debt against default has also risen.

Despite maintaining China’s “A1” long-term local and foreign-currency issuer ratings, Moody’s anticipates the country’s annual GDP growth to slow down significantly in the coming years, with projections of 4.0% growth in 2024 and 2025, and an average of 3.8% from 2026 to 2030. This outlook revision comes ahead of the Central Economic Work Conference (an annual meeting held in China which sets the national agenda for the economy and the country’s financial and banking sectors), where advisors will likely call for a steady growth target for 2024 and increased stimulus.

Analysts note that the A1 rating remains high in investment-grade territory, and the downgrade will not trigger forced selling by global funds. But still, it is a significant change.

The Chinese economy’s struggle to mount a strong post-pandemic response has been exacerbated by various factors, including the crisis in the housing market, local government debt concerns, slowing growth, and geopolitical tensions. These have collectively dampened the momentum of the economy, which is continuing to decelerate from its historic phase of rapid expansion.

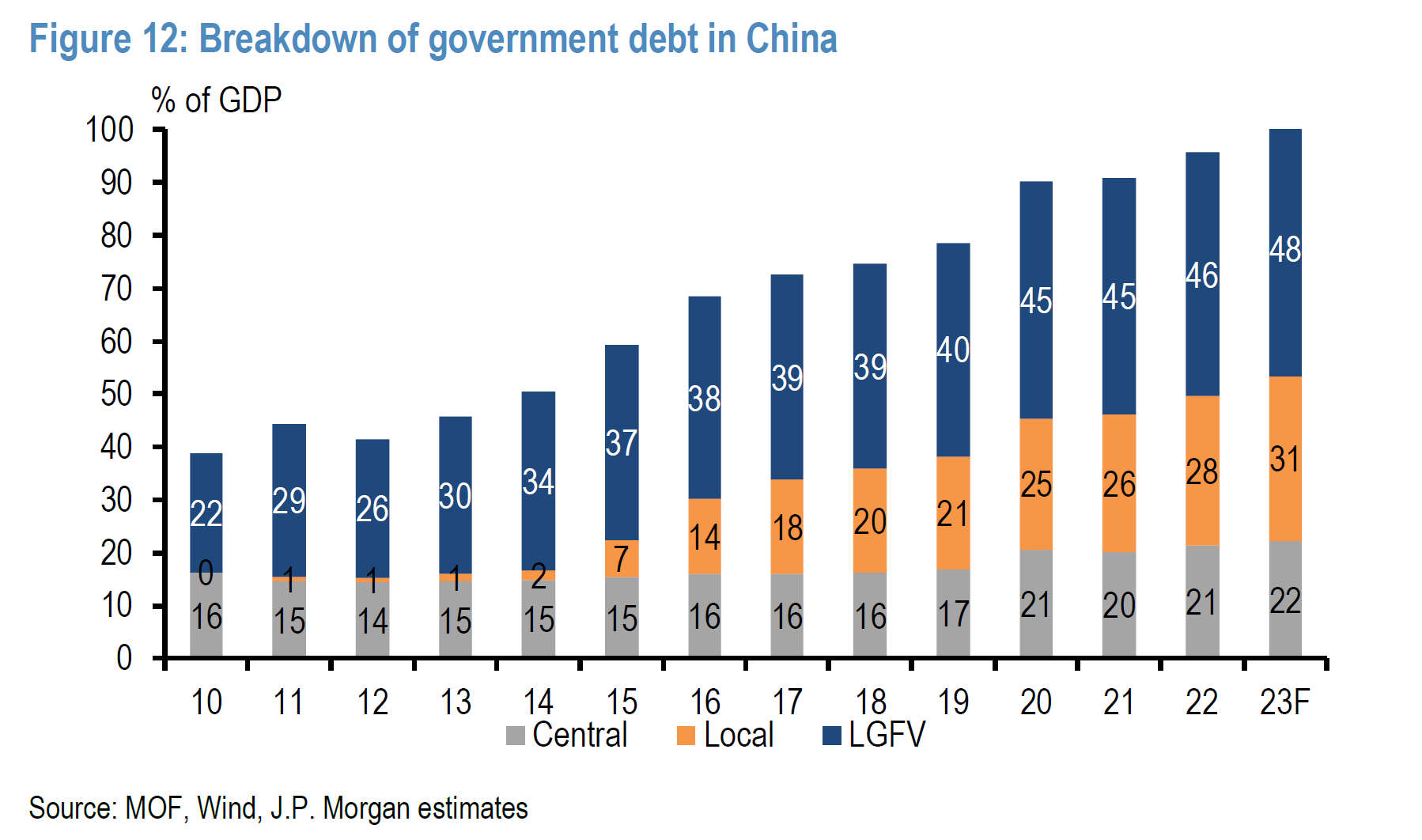

Local Government Debt

China is grappling with a hidden debt crisis as local governments -- cities and provinces -- have accumulated off-balance-sheet government debt estimated at $7 trillion to $11 trillion. To address the issue, Chinese authorities are swapping hidden debt for new government debt; local governments are urged to issue special refinancing bonds to replace off-balance-sheet debt, with about $200 billion raised so far. Experts believe that a more substantial debt swap of around $700 billion may be needed to resolve the hidden debt problem.

JP Morgan recently wrote an extensive report on China’s LGFV debt problem, estimating this debt has grown to over 60 trillion renminbi, and represents almost half of China’s government debt.

Source: Morgan Stanley Research

This problem has been apparent for many years, but seems finally to be coming closer to a boiling point. Analysts long assumed that debt taken on by localities would eventually make its way to the central government’s balance sheet. The reason that may be problematic is described below. The imbalances create the specter of an intolerable currency crisis, and in response to that threat, China is intensifying its efforts to isolate its financial system from the rest of the globe -- efforts that we think are ultimately doomed to failure.

Key Economic Concerns

Historically, China was known for its robust economic growth and integration into the global market; however, in the last decade, the Chinese government’s emphasis on maintaining a stable currency has led to an enormous accumulation of domestic money supply. As a preventive measure against destabilization caused by internal debt problems, and against capital flight from China as corrupt oligarchs try to move their wealth to the west, China has increasingly resorted to financial isolation, limiting both incoming and outgoing financial flows.

Symptoms of the Problem

This is evident in various economic policies and practices. For instance, there has been a noticeable tightening of controls over remittances by households and businesses. The government has also imposed stringent restrictions on fundraising activities and set quotas on imports. Though they have a political dimension, these actions are more primarily economic, aiming to control the domestic financial ecosystem and prevent the externally originating economic shocks that periodically trouble more open developing-market economies.

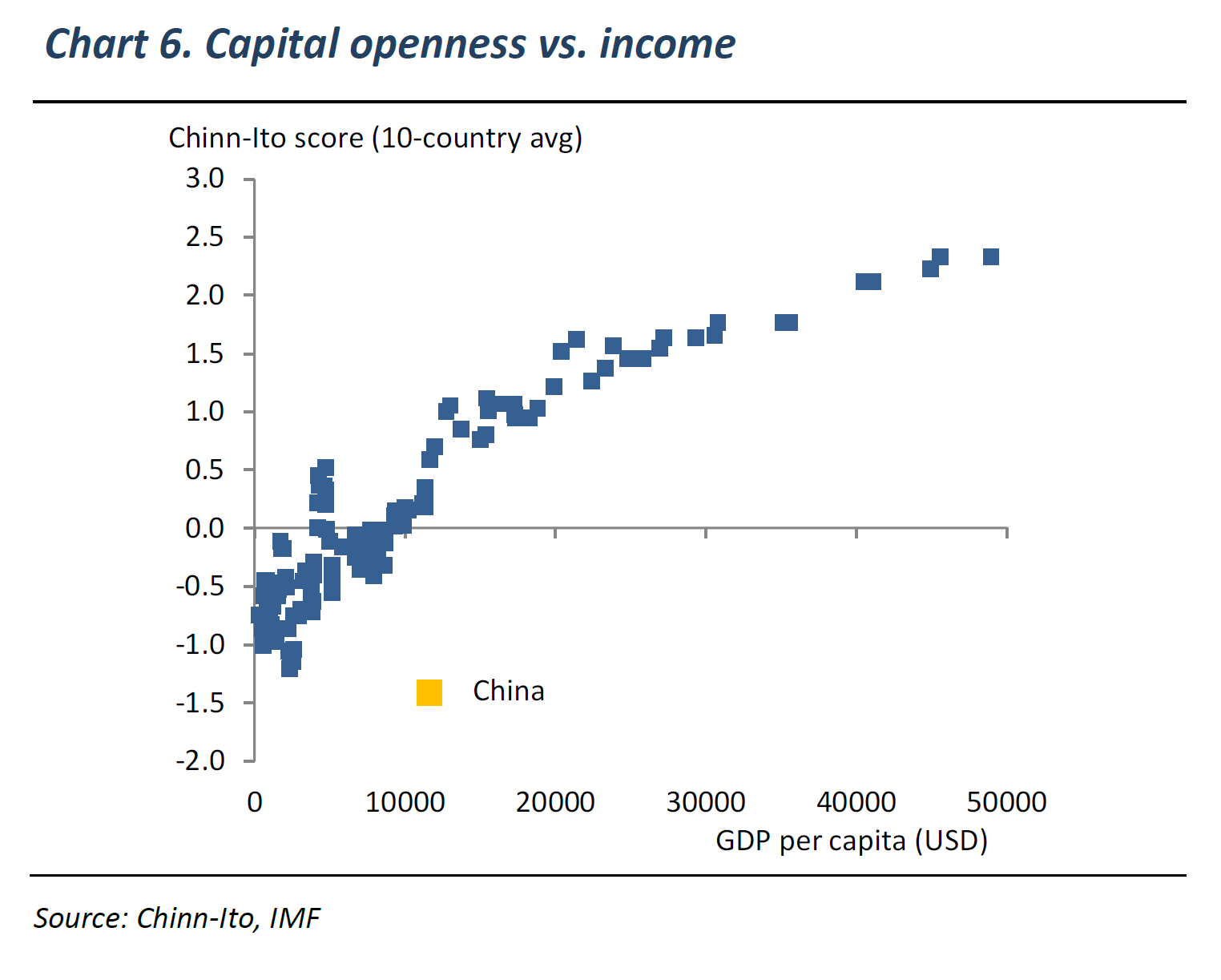

China’s Financial Landscape

China commands a substantial portion of world GDP and international trade. Despite this, as we have described in many letters, the country has maintained a financial system that is far more tightly closed than other global economies its size. The Chinese currency plays a minimal role in global foreign exchange markets (nor can it as long as the Chinese regime maintains total domestic control). Furthermore, the foreign ownership of Chinese assets is surprisingly low -- far lower than it should be given the country’s global economic importance -- showing the limited characters of China’s international financial integration.

A closed capital account, where a country restricts the flow of capital across its borders, is nothing new. However, China’s approach stands out for its rigidity, and for its persistence given the growth and influence of the Chinese economy. It is a profound outlier in the trajectory of opening that typically occurs as countries advance along the path of economic development. Its closed capital account is one of the most restrictive among major global economies.

Source: Emerging Advisors Group

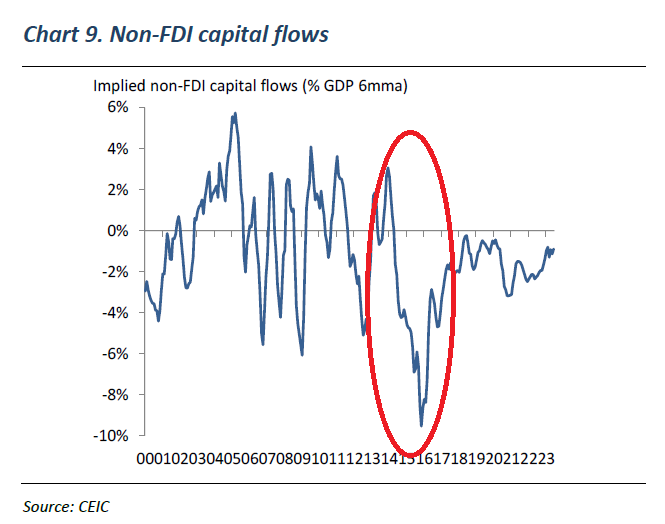

Recent Developments and the 2015 Turning Point

2015 marked a turning point in China’s economic history. The country, which had consistently seen a surplus in its balance of payments, began experiencing massive capital outflows. These outflows were so significant that they prompted the government to initiate a regime of tighter financial and capital controls, in order to curb the sudden and substantial outflow of money -- which could have led to severe economic instability or a currency crisis. This was two years after Xi Jinping’s accession to power; it is hard to avoid the conclusion that his political adversaries -- mainly the competing oligarchic blocs of previous leaders, their political coteries, and their children -- were working overtime to get their wealth somewhere beyond the new regime’s reach.

Source: Emerging Advisors Group

Impact on Current Account Transactions

Notably, China’s restrictions have extended beyond capital account transactions to current account transactions, which typically include trade in goods and services. There has been a deliberate slowing down in the growth of import volumes, and restrictions have been placed on international travel and tourism expenditures. These measures, though economic in nature, reflect the government’s intent to control the flow of money and safeguard their control of the economy against external vulnerabilities.

No Credible Exit Strategy

One of the most challenging aspects of China’s current economic policy is the lack of a feasible exit strategy. The large volume of domestic liquidity -- large and growing rapidly in response to mounting internal pressures -- poses a significant challenge. Opening up the economy to global financial flows would destabilize the currency; this is an eventuality we have often referred to when we suggest that the renminbi is vulnerable to a severe and chaotic decline within the next five years.

The delicate balance between maintaining currency stability and supporting economic growth makes it exceedingly difficult for China to reverse its path towards financial isolation without encountering substantial economic disruptions. Eventually, China will learn a hard lesson about capitalism: namely, that every form of capitalism is vulnerable to stresses beyond its control, and cannot exist and develop without periodic crises of one sort or another -- and the more draconian the attempts to clamp down on the emerging stresses, the more problematic the ultimate resolution is likely to be.

Conclusion

China’s journey from the pursuit of global integration (on its own terms, to be sure) to a stance of isolationism (coupled with a certain geopolitical belligerence, as is often the case during such a transition) is a significant development. While the country’s policy goals have often been aligned with a form of global economic integration, its recent practices tell a rather different story. This shift towards deeper financial, economic, and geopolitical isolation has profound implications for the future of China’s economy.

Because of the relatively minor size of China’s equity market compared to the Chinese economy, it is driven much more by sentiment and liquidity than by fundamentals. While we caution against any strategic commitment to Chinese equities, they can make tactical sense, but only when momentum shows that domestic speculative appetite is active. Current developments continue to reinforce our view that investment exposure to China should be a short-term proposition with a tight stop.

Finally, we’ll reiterate what we wrote two weeks ago: “Many of the shares of Chinese companies that trade as ADRs on U.S. exchanges are in fact issued by variable interest entities (VIEs) domiciled in jurisdictions that are not known for the easy availability of legal redress for investors. In short, when you own such a security, you should not think that you own a share of a company in the direct way you do when you own a U.S., European, or Japanese stock.”

Thanks for listening; we welcome your calls and questions.

General Disclosures About This Newsletter

The publisher of this newsletter is Guild Investment Management, Inc. (GIM or Guild), an investment advisor registered with the Securities and Exchange Commission. GIM manages the accounts of high net worth individuals, trusts and estates, pension and profit sharing plans, and corporations, among other clients.

Your receipt of this newsletter does not create a personal investment advisory relationship with GIM although some recipients may also be advisory clients of GIM. GIM has written investment advisory agreements with all its personal advisory clients, which sets forth the nature of that relationship.

The newsletter makes general observations about markets and business and financial trends and may provide advice about specific companies and specific investments. It does not give personal investment advice tailored to the needs, objectives, and circumstances of individual readers. Whether investment ideas and recommendations are suitable for individual readers depends substantially on the personal and financial situation of that reader, which GIM, as the publisher of the newsletter, makes no effort to investigate.

GIM attempts to provide accurate content in its newsletters to the extent such content is factual rather than analysis and opinion, but GIM relies primarily on information compiled or reported by third parties and does not generally attempt to independently verify or investigate such information. Moreover, some content and some of the assumptions, formulas, algorithms and other data that affect the content may be inaccurate, outdated, or otherwise flawed. GIM does not guarantee or take responsibility for the accuracy of such information.

Please note that investing in stocks, other securities, and commodities is inherently risky, and you should rely on your personal financial advisors and conduct your own due diligence in connection with any investment decision.

A Special Comment for Guild’s Clients

If you are an investment advisory client of GIM who is receiving this newsletter, please note that the fact that a general recommendation is made of a particular security, commodity, or investment area to its newsletter subscribers does not mean that investment is suitable for you or should be purchased by you. For example, GIM may already have purchased such securities on your behalf or purchased securities in the same industry (and an increase in the position for you may represent too much concentration in one security or industry), or GIM may believe the investment is not suitable for you based on your risk tolerance or other factors. If you have questions about the recommendations in this newsletter in relation to your account at GIM, please contact Tony Danaher, Rudi von Abele, or Aubrey Ford.

Conflicts of Interest

As of the date of this newsletter, GIM’s investment advisory clients or GIM’s principals owned positions in areas that are the subject of current recommendations, commentary, analysis, opinions, or advice, contained in this newsletter.

GIM and its principals have certain conflicts of interest in its relations with its investment advisory clients and its newsletter subscribers resulting from GIM or its principals holding positions for its clients or themselves which are also recommended to its clients. GIM may change the positions of its clients or GIM’s principals may change their positions (increasing, decreasing, and eliminating them) based on GIM’s best judgment at any given time, including the time of publication of the newsletter. Factors that lead GIM to change or eliminate its positions may include general market developments, factors specific to the issuer, or the needs of GIM or its advisory clients. From time to time GIM’s investing goals on behalf of its investment advisory clients or the personal investing goals of GIM’s principals and their risk tolerance may be different from those discussed in the newsletter, and the investment decisions made by GIM for its advisory clients or the investment decisions of its principals may vary from (and may even be contrary to) the advice and recommendations in the newsletter.

In addition, GIM or its principals may reduce or eliminate their positions in an investment that is recommended in the newsletter prior to notifying the newsletter subscribers of such a reduction or elimination. The publication by GIM of a “target price” or “stop loss” for a particular security or other asset does not necessarily represent the price at which GIM intends to sell or will sell any such assets for its advisory clients or the price at which GIM’s principals intend to sell any such assets.

As a consequence of the conflict of interest, GIM’s clients or principals may benefit if newsletter subscribers purchase assets recommended by GIM since it could increase the value of the assets already held by GIM’s investment advisory clients or GIM’s principals. On the other hand, GIM’s principals and clients may suffer a detriment if they seek to acquire additional shares in securities that have been recommended and the price of the securities has increased as a result of purchases by newsletter subscribers.

To help mitigate these conflicts, GIM seeks to avoid recommending the securities of individual companies where GIM or its principals have an ownership position and where the issuer is small or its securities are thinly traded. That way sales by GIM in advance of possible sales by newsletter subscribers would not be likely to cause any significant decrease in the sale price to newsletter subscribers. GIM has a fiduciary relationship with its investment advisory clients and cannot agree on behalf of such clients to refrain from purchases or sales of a security mentioned in the newsletter for a period of time before or after recommendations for purchases or sales are made to its newsletter subscribers.

GIM encourages you to do independent research on the securities or other assets discussed or recommended in the newsletter prior to making any investment decisions and to be especially cautious of investments in small, thinly-traded companies, which are usually the most risky investments that you can make.

Disclaimer of Liability

GIM disclaims any liability for investment decisions based upon recommendations, information, or opinions in its newsletters. GIM is not soliciting you to execute any trade. Nothing contained in GIM’s newsletters is intended to be, nor shall it be construed as an offer to buy or sell securities or to give individual investment advice. The information in the newsletter is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject GIM to any registration requirement within such jurisdiction or country.

COPYRIGHT NOTICE

Guild’s current and past market commentaries are protected by U.S. and International copyright laws. All rights reserved. You must not copy, frame, modify, transmit, further distribute, or use the market commentaries, without the prior written consent of Guild. This email or any download from a secure website is meant for only the intended recipient of the transmission, and may be a communication privileged by law. If you received this email in error, any use, dissemination, distribution, or copying of this email is similarly prohibited. Please notify us immediately of the error by return email and please delete this message from your system. Although this email and any attachments are believed to be free of any virus or other defect that might affect any computer system into which it is received and opened it is the responsibility of the recipient to ensure that it is virus free and no responsibility is accepted by Guild Investment Management for any loss or damage arising in any way from its use.